Is Albert legit? A closer look at the financial app

Albert is generally considered a legitimate financial app. It’s designed to help track spending, bills, and savings. The platform implements security protocols to keep users’ information safe, and partners with FDIC-insured banks to hold users’ funds.

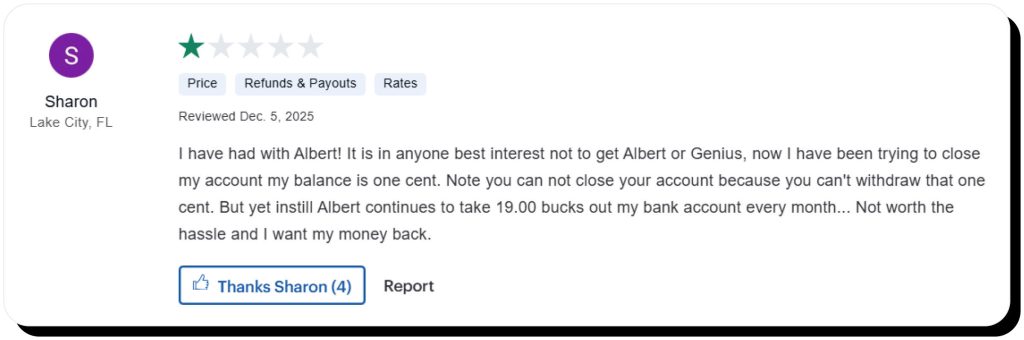

However, some people have reported issues with customer service and difficulties with cancelling a subscription. The latter is typically due to the strict policy of having a $0 balance across all Albert products to be eligible to close an account.

What is the Albert app?

Albert is a personal finance app that provides budgeting tools and automatic savings features. Some plans also include financial assistance, credit score monitoring, and cash back rewards.

Importantly, Albert is not a bank and doesn’t hold any money. It’s a fintech company that partners with FDIC-insured banks, including Wells Fargo and Stride Bank.

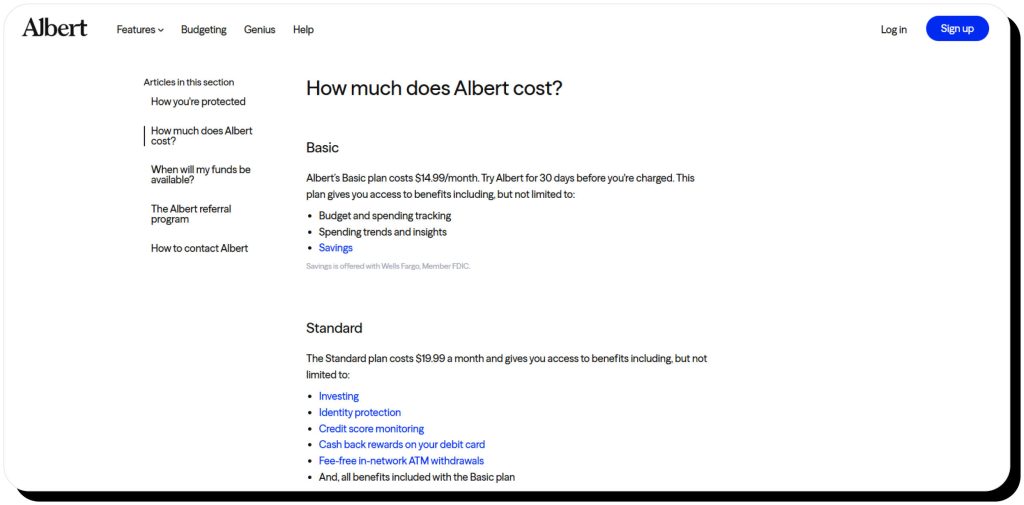

The app is free to download, but most features require a subscription, with costs currently ranging from $14.99/mo to $39.99/mo.

Is the Albert app legit?

Albert is a legitimate company headquartered in Los Angeles, CA, and operating legally in the United States. It was founded in 2015 with the mission to help everyone achieve financial stability. Over the years, the company has formed strategic partnerships and raised money, including a $100 million Series C funding from General Atlantic.

Albert earns revenue from its monthly subscription service as well as interchange fees when users spend with the Albert debit card. Additionally, the company generates income through interest on idle funds held in partner bank accounts and may receive referral fees from promoting third-party financial products or services within the app.

Is Albert safe to use?

As long as you take common precautions related to online banking, Albert is safe to use: it implements security protocols to safeguard users’ personal and financial information. Also, Albert partners with FDIC-insured banks to protect users’ funds.

Security measures

Data encryption

Albert uses Secure Sockets Layer (SSL) encryption to create a secure connection between users’ devices and the app’s servers. This ensures that login credentials and other sensitive details can’t be intercepted by third parties.

Login protection

Every user is required to set up a password for their account. In addition to that, the following options can be enabled:

- Face ID

- Touch ID

- PIN

Read-only bank access

Albert is set to “read-only” mode for linked bank accounts. This means that the app can only view your balance, transactions, and income history—it can’t move or withdraw your money.

Moreover, Albert doesn’t have access to the login credentials to your banking accounts. The app uses a trusted intermediary, Plaid, to connect to your bank and transmit read-only financial data using encrypted channels.

Monitoring for suspicious activity

Albert monitors accounts for suspicious activity 24/7. Some plans also include dark web monitoring and alerts if a new financial account is opened with your personal information.

FDIC insurance explained (and its limits)

Albert stores users’ funds in FDIC-insured partner banks. This means that if a partner bank fails, the Federal Deposit Insurance Corporation (FDIC) guarantees the return of your funds up to $250,000 per depositor, per bank.

It’s important to note, however, that it protects your balance from bank insolvency—not from fraud, investment losses, or unauthorized access.

Is the loan feature legit?

Albert offers two options when it comes to loans: Instant Advance and Instant Loan. Both are legitimate but differ in limits and requirements:

- Instant Advance: This option allows users to take an advance of $25-$1000 with no credit check, late fees, or interest. It’s also non-recourse, meaning Albert can’t pursue legal action or force repayment if a user is unable to pay back. That said, advances are expected to be repaid within 6 days and failure to do so will result in suspension of some features.

- Instant Loan: This is essentially a traditional loan. When users apply, Albert requests a credit pull and determines an amount between $1,000 and $5,000. Once approved, customers can access the money immediately either in their Albert Cash account or transfer it into an external account. Loans are fixed interest rate and unsecured (you don’t need to provide collateral like upfront payments or personal assets).

What do the Albert app reviews say?

When it comes to public opinion about Albert, the reviews are mixed.

Some platforms have very unfavorable ratings. For example, on ConsumerAffairs, Albert currently has a score of 1.2 out of 5 stars. The issues that are most often raised by customers include:

- Surprise withdrawals

- Trouble closing accounts

- Difficulty reaching customer service representatives

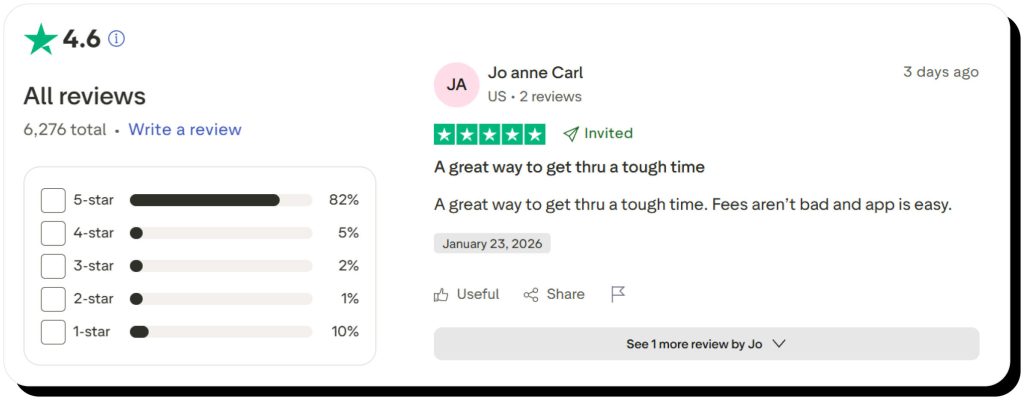

On the other hand, ratings on other platforms are more favorable:

- Google Play: 4.5 out of 5 stars

- App Store: 4.6 out of 5 stars

- Trustpilot: 4.5 out of 5 stars

Reviews note that the app is easy to use, especially when it comes to budgeting and saving automatically. Many praise the Instant Advance feature, stating it helped them in emergency situations.

How to use Albert safely

To protect your personal and financial information, follow these best practices:

- Avoid using the app when connected to public Wi-Fi: Otherwise, your sensitive data like login credentials could be intercepted by hackers.

- Examine the Terms before buying a subscription: Make sure you understand the conditions to avoid surprise charges.

- Safeguard your account with biometrics or PIN: These add a higher level of security than a password as the latter can be cracked or breached.

- Monitor your bank accounts: Even though Albert monitors your financial accounts, it’s a good habit to regularly check for any signs of unauthorized activity yourself.

- Adjust settings to limit data sharing: Manage the permissions that the app has to avoid access to data it doesn’t need to operate.

- Be mindful with cash advances: Only use cash advances when necessary and ensure you’ll be able to repay them on time.

- Avoid linking your primary bank account: Use one with limited funds in case you can’t easily cancel a subscription and charges continue.

FAQs

Is Albert loan legit?

The Albert app provides two legitimate options: cash advances and loans. Cash advances don’t require a credit pull and are available for a range of $25-$1,000. Loans require a credit pull and the available range is $1,000-$5,000.

Is Albert a good app?

Albert can be helpful for people who have trouble managing money on their own. The app can track costs and subscriptions, helping people identify unnecessary spending. However, the app itself can present financial risks, as subscription costs can add up and surprise withdrawals may trigger overdraft fees.

Mark comes from a strong background in the identity theft protection and consumer credit world, having spent 4 years at Experian, including working on FreeCreditReport and ProtectMyID. He is frequently featured on various media outlets, including MarketWatch, Yahoo News, WTVC, CBS News, and others.