Is Perpay legit? How it works, real costs, and what to watch out for

Buy now, pay later (BNPL) has become a financial lifeline for many Americans. A January 2025 report from the Consumer Financial Protection Bureau found that more than 21% of consumers with a credit record used a BNPL loan in 2022, with most borrowers having subprime or lower credit scores. Nearly two-thirds carried multiple BNPL loans at the same time.

With rising prices and limited access to traditional credit, services like Perpay promise access to products today and automatic payments through your paycheck.

Perpay offers the same convenience as many BNPL companies, but not always at an affordable price. Its payroll-based model raises important questions about cost, control, and risk.

So, is Perpay legit — and is it worth using? In this guide, we’ll break down how it works, what real users say, the true costs involved, and the red flags to watch for before signing up.

What is Perpay?

Perpay is a US-based financial platform that lets you buy things now and pay for them later in installments. It may be a solid option if you have a low credit score or no credit history but earn a regular income.

The company offers 2 different products:

- Perpay marketplace. A platform where you can purchase a variety of products, including tech, home goods, clothes, and more. If you choose to pay for the optional credit-building feature (Perpay+), you can even boost your credit score by shopping and paying off products.

- Perpay credit card. A Mastercard for those who want more than just the Perpay marketplace. It works like a standard unsecured credit card: needs monthly automatic payments from your account and builds up your credit score.

How does Perpay work?

Let’s take a closer look at how Perpay works.

Step 1: Sign up and get a spending limit

You start by creating a Perpay account and providing basic personal and payroll information. Once approved, you receive a spending limit that determines how much you can use in the Perpay Marketplace or, if eligible, on the Perpay credit card.

Unlike traditional lenders, Perpay primarily bases your limit on your income and payroll history rather than a standard credit score check.

Step 2: Set up a split direct deposit

Next, you’ll have to link your bank account to Perpay and set up the exact amount that will be deposited to your Perpay balance. The payments are automatically deducted on a date that works best for you, usually scheduled around when you get paid. Of course, it will typically be just a small part of your paycheck.

The split direct deposit covers your Perpay marketplace purchases (if any) and your credit card balance (if you have one). Now, onto the unpleasant surprise. Direct deposits will continue even if you haven’t used your card at all and didn’t buy anything from the marketplace. The money is, of course, not lost, but you have to use it through Perpay.

If you switch jobs or payroll providers, update your deposit settings to keep using the platform.

Step 3: Choose how you’ll use it

Once you get everything set up, you should be good to go. You can either buy goods on the Perpay marketplace or apply for the Perpay credit card, which you can use anywhere Mastercard is accepted.

Step 4: Ordering on Perpay Marketplace and “when does it ship?”

Excited to make your first order? Before you do, there are a few things you should know.

Orders ship after your first direct deposit. So, you technically have to pay a part of the total before getting the products. Shipping tends to take a bit more time for new users. If you’ve been using the platform for a period, you’ll see the orders arriving quicker.

If your order hasn’t been shipped yet, don’t worry. Check the following:

- What’s your order status in the dashboard? It might still be processing.

- Has your first deposit been cleared? If not, wait for it to go through.

- Has Perpay emailed you to ask for verification? Sometimes you’ll need to confirm the details.

If you see no apparent issues and shipping is still delayed, it might be time to reach out to Perpay customer support.

Is Perpay legit and safe to use?

Yes, Perpay is a real and legitimate company. It reports payments to the three major US credit bureaus, partners with employers and payroll systems, and its website adheres to standard security protocols.

Also, the business is BBB accredited and rated with an A+, which means that it has a strong record of resolving customer issues. But that doesn’t mean there aren’t mixed reviews, just like with any other service.

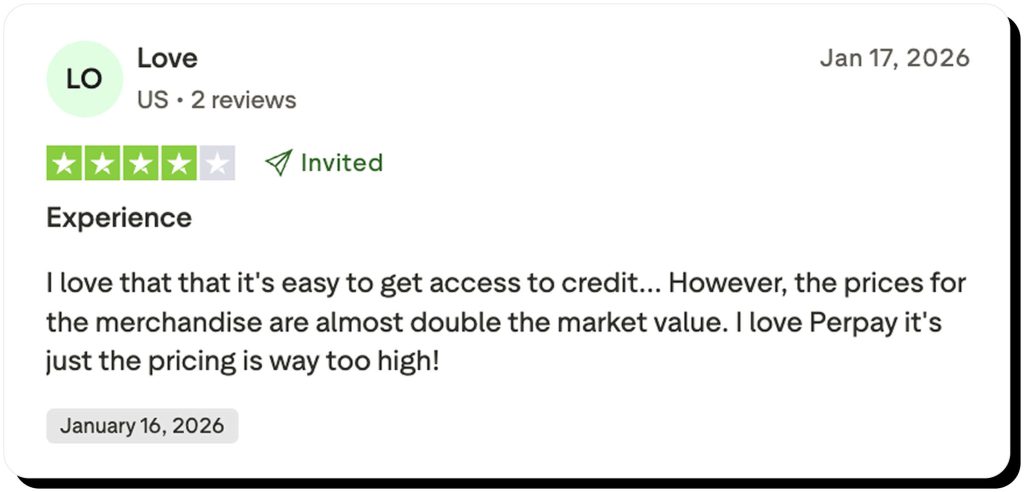

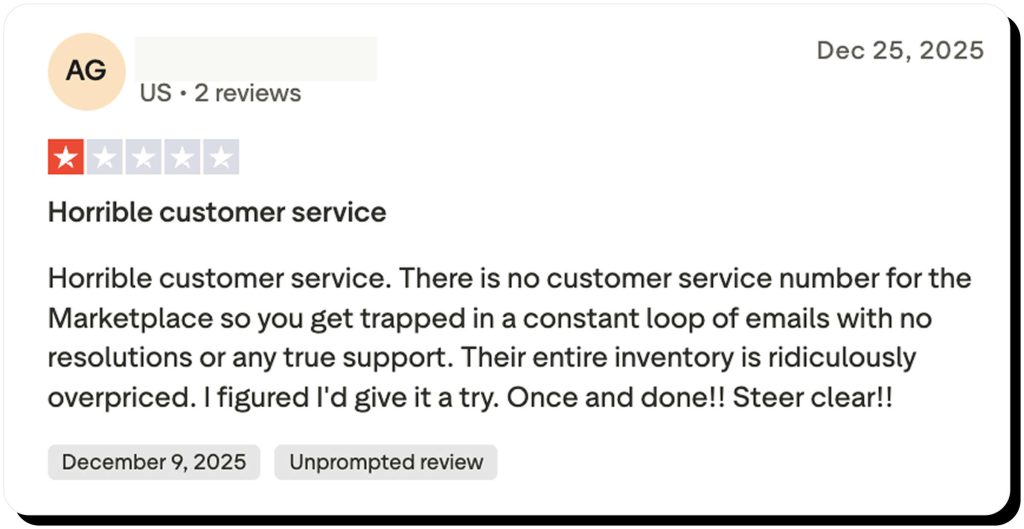

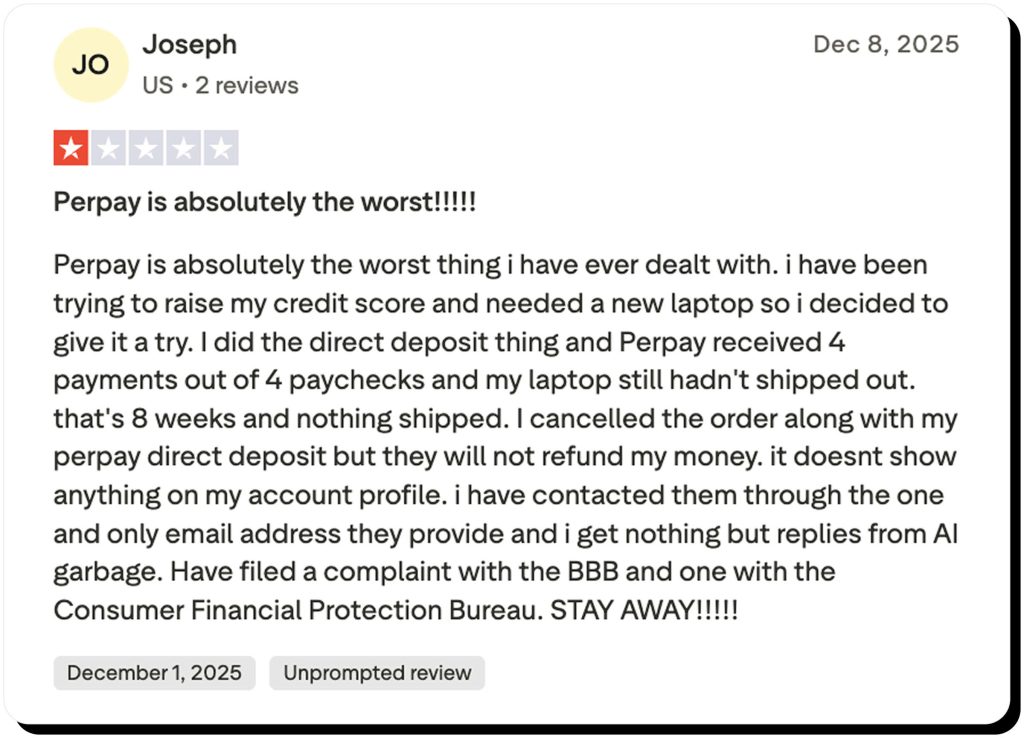

If you search through public review forums, you’ll find a bunch of Perpay reviews. Trustpilot alone collects over 3000, and 77% of them are 5-star. The overall platform rating is 4.6, which is high, but there are still people who report negative experiences.

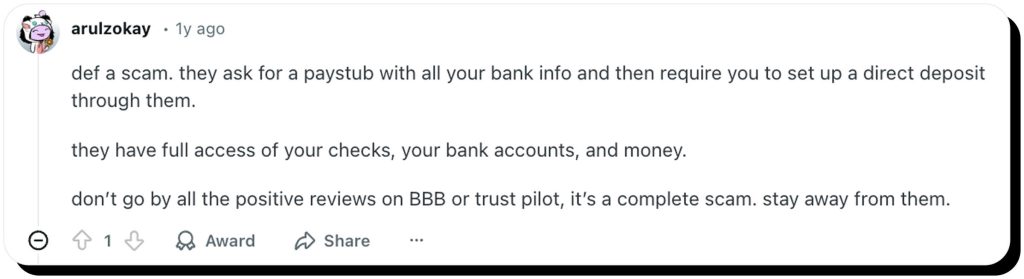

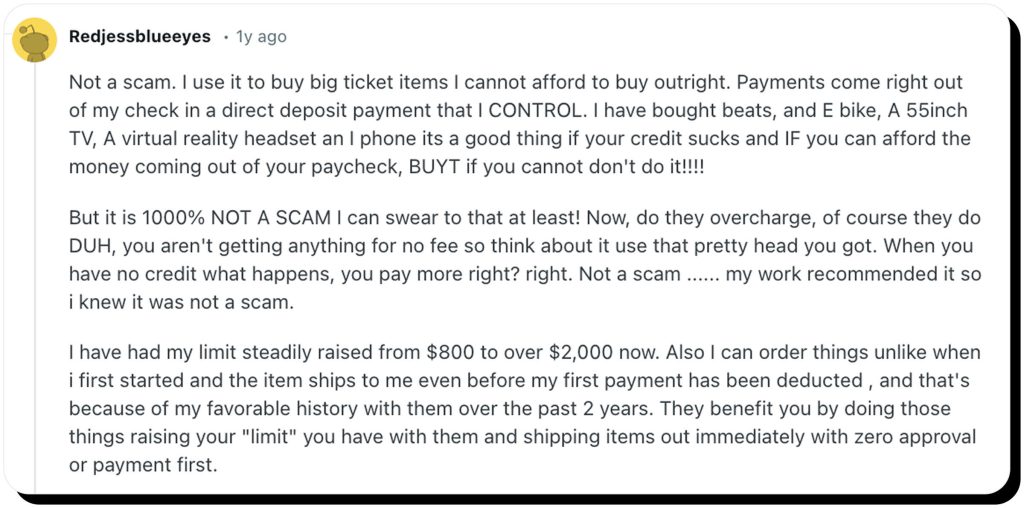

Why does Perpay feel like a scam to some?

Some users have doubts about Perpay, mainly because they misinterpret the following as red flags:

- Linking a paycheck. The split direct deposit can feel odd if you’re used to regular credit cards, but it’s an extra safety precaution for Perpay.

- Marketplace prices. Perpay does sell goods at a higher markup on its marketplace. But that’s not unusual for buy-now-pay-later models.

- Big marketing promises. A lot of Perpay marketing is centered around fee-free buying and helping you boost your credit score. Marketplace purchases don’t carry hidden fees, but credit card plans do come with interest. Building credit while you shop is possible, too, but it might take a bit more time and consistency.

Can using Perpay become a real issue?

Yes, according to Perpay reviews, things can go wrong in some cases:

- You don’t fully understand the credit card terms and fees before applying for it

- Customer support is not able to resolve your problem

- It takes a long time to return stuff and get a refund on the marketplace

- You rely on Perpay for purchases you can’t realistically afford

What does Perpay really cost?

Marketplace markup

When shopping on the Perpay marketplace, you pay zero interest. But there might be a more obscure fee: most products are priced at a higher markup than elsewhere.

Before you commit to Perpay, do the 60-second price check. Google the item and check the price on Walmart, Amazon, or Best Buy. If the Perpay total is much higher, consider if it’s really worth it.

Fees and APR

The Perpay credit card works in a similar way to classic credit cards.

In essence, you pay:

- A one-time $9 account opening fee

- $0 annual fee, but $9 monthly servicing fee (~$108/year)

- Around 29.49% APR if you don’t pay your balance in full by the due date

Perpay credit card does NOT divide the total into installments, as the marketplace does. And you’ll be paying the monthly deposit regardless of whether you use the card.

A quick “is it worth it?” cost test

Do you want to buy an expensive piece of tech, or do you need a credit card to buy groceries? Perpay can be a sound financial choice in the first case, and questionable in the other.

If you buy things at a small markup on the marketplace and manage to pay off your credit card monthly, Perpay works as a charm. If that’s not the case, take a minute to ask yourself:

- On the Perpay marketplace, what’s the total I’ll be paying? If the item price is at a much higher markup, consider getting it somewhere else.

- When it comes to the credit card, am I certain I can avoid paying interest? The Perpay credit card comes with a pretty high interest rate (almost 30%), so you might be better off using something else.

Pros and cons of using Perpay

As with any other service, there’s the good and the bad. Consider all factors before you sign up.

| Pros | Cons |

|---|---|

| Automatic payments. You pay by automatic paycheck split deposit, so there’s no way you can miss a due date. | Marketplace markup. Some products cost more than at major retailers. |

| Access without perfect credit. Banks tend to find anyone with low credit undesirable, but Perpay relies on income and payroll stability. | Fees, especially with the credit card. Opening fees, monthly service fees, and interest (if you carry a balance) can add up. |

| Potential credit-building. Paying off your balance on time will help you build credit. | Payroll problems. Changing jobs or payroll providers can make you ineligible for Perpay. |

Where can you use Perpay?

Perpay Marketplace vs Perpay credit card

Perpay’s main offering is the marketplace. If you want to shop somewhere else, you’ll have to request the Perpay credit card. The card works wherever Mastercard is accepted.

Does Amazon accept Perpay?

Unfortunately, Amazon is not connected with the Perpay marketplace. You can still shop there using a Perpay credit card, as it works just like any other Mastercard.

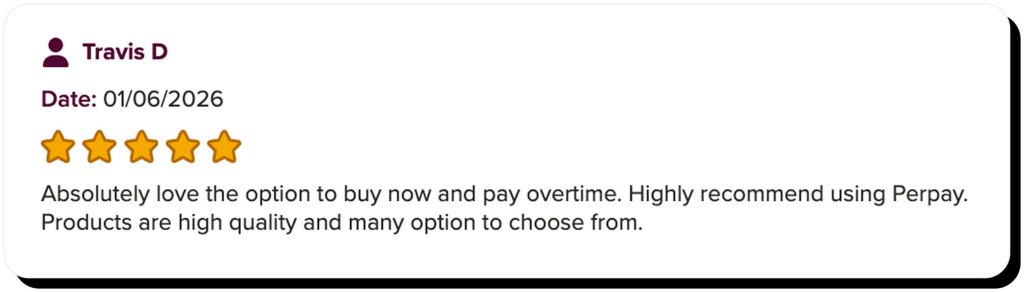

Perpay reviews and real user feedback

When looking at reviews, don’t focus on just the rating and individual comments. Read both positive and negative reviews and try to detect common themes.

For example, the reviews confirm that Perpay is not a scam, but it can be expensive. Many people found the platform to be convenient, especially for big, expensive purchases. Others liked the credit reporting option.

On the flip side, some users were frustrated by shipping delays and not being able to resolve issues through customer support. Many pointed out that pricing is a little confusing, and weren’t sure how deposits or withdrawals worked.

Red flags and scam lookalikes to avoid

Fraudsters impersonate legitimate financial companies, including Perpay. They can be creative and come up with elaborate schemes:

- Phishing emails or texts that sound urgent, such as your account getting locked. Pause and think before clicking on links and entering your login credentials.

- Fake support numbers may appear online. Remember that Perpay only uses direct channels of communication.

- Pretend Perpay agents may reach out to people via social media, texts, or calls. The goal is to get you to reveal sensitive information.

If you fall for a scam, your Perpay account can be compromised. You may notice that something is off by unrequested password reset emails, changes to your payment method and payroll settings, or purchases you didn’t make. Worst-case scenario, you might get locked out of your account.

Act quickly if you notice red flags.

- Change your password right away and enable two-factor authentication (2FA).

- Check your accounts for unauthorized charges.

- Monitor your bank and credit activity.

- Contact Perpay customer support.

Read more:

Venmo scams: how to recognize, avoid, and recover from fraud

Zelle scams: how they work and how to stay safe

Cash App scams: how to spot, avoid, and recover from them

Apple Pay scams: how to spot and avoid them

Alternatives to Perpay

Is Perpay good for people with low credit scores? Yes. Could there be other, perhaps better options? Absolutely.

- Pay-in-4 BNPL: Some financial companies, like Klarna or PayPal, offer a payment model that automatically splits your purchase into 4 installments. Payments are usually made every 2 weeks, and there may be no interest if you pay on time.

- Retailer financing/installment plans. Stores often have their own payment plans that let you pay off stuff over several months.

- Secured or credit-builder cards. There are special credit cards for people building or rebuilding their credit. The concept is simple: the deposit you place becomes your spending limit.

- Credit union small loans. Credit unions may offer “credit-builder” loans to their members. These often have lower interest rates and more flexible terms, but aren’t available to everyone.

Privacy and safety tips before you sign up to BNPL services

Treat your payroll and direct deposit details as highly sensitive information. While Perpay has security measures in place, your personal safety online also depends on the habits you build.

- Start with the basics: use a strong, unique password and enable two-factor authentication (2FA) wherever possible.

- Before creating an account, double-check that you’re on the official Perpay website or app — not a lookalike page designed to steal your information.

- Be cautious of anyone claiming to be a Perpay representative who contacts you unexpectedly about special offers, perks, or account issues. These scams can feel convincing, especially when the caller or sender already knows your full name, address, or phone number. In many cases, that information isn’t stolen from the company itself — it’s pulled from data brokers and people-search websites where personal details are publicly listed.

Reducing the amount of personal information available about you online can make these scams much less effective.

How Onerep can help protect your privacy online

Removing your information from data broker and people-search sites can help reduce privacy risks and avoid phishing emails, fake support calls or identity fraud. However, doing it manually isn’t always simple. Each website has its own opt-out process, verification steps, and follow-ups. Opt-outs can take days — and your data may reappear later.

Onerep simplifies this process. We scan 318 data broker and people-search websites to identify where your information is listed and submit removal requests on your behalf. To keep you protected during opt-outs, we use temporary email addresses and phone numbers so your real contact details aren’t further exposed.

The less personal information available about you online, the harder it is for scammers to use it against you.

FAQs about Perpay

Is Perpay worth it?

This is a very personal question, depending on your budget and need for flexibility. Perpay can be useful if you need flexible payments while building your credit. But, you often end up paying a larger sum than you would’ve for one-time payment. There could be other options, too.

Does Perpay take your whole paycheck?

No, Perpay doesn’t take your whole paycheck. You automatically pay a deposit that you agree on when signing up, at a convenient date.

Does Perpay sell real items?

Yes, Perpay marketplace offers real products, including electronics, appliances, and other household items.

H3: Do you need direct deposit for Perpay?

Yes, you need to link your checking account and Perpay will automatically deduct payments.

Is Perpay monthly or weekly payments?

It depends on your pay schedule. Payments are always spread across multiple periods, often biweekly or monthly.

Can you cancel a Perpay account?

Yes, you can, but you need to pay off your entire balance first. Make sure all active orders are completed or transferred before canceling to avoid disruptions

Mark comes from a strong background in the identity theft protection and consumer credit world, having spent 4 years at Experian, including working on FreeCreditReport and ProtectMyID. He is frequently featured on various media outlets, including MarketWatch, Yahoo News, WTVC, CBS News, and others.