Unifin debt collector text: how to tell if it’s a scam or legitimate

Who is Unifin, a debt collector, and is it legit? These questions are common as people report getting Unifin texts they suspect are a scam.

Even though Unifin is a legitimate U.S.-based debt collection agency, scammers frequently impersonate it to make people pay “debts” they don’t owe or give away sensitive information out of fear of ruining their credit score or facing a lawsuit.

This guide will walk you through the common signs of Unifin scam texts and ways to protect yourself if you ever receive one and wonder whether you should act or ignore it.

What is Unifin Inc.?

Is Unifin legit? Yes, Unifin Inc. is a legitimate U.S.-based debt collection and business process outsourcing company with headquarters in Skokie, IL. Established in 2011, it is veteran-owned and operates several contact centers across the USA, Latin America, Africa, and Asia.

To further confirm its legitimacy, Unifin is a licensed collection agency and is a BBB accredited business.

Similar to many other companies in the field, Unifin contacts consumers on behalf of its clients (original creditors) to help them recover unpaid debts and manage overdue accounts, sometimes years after the original debt originated. Unifin also acquires old and outstanding debts from other companies and agencies in a process known as debt transfer.

Who does Unifin collect for? As an authorized third party, Unifin collects debts for credit card issuers, banks, healthcare providers, and other lenders. This means that when you get a text or a call from Unifin, you may not recognize the organization, but it may still reference a legit outstanding debt you owe to the original lender.

Why did you receive a Unifin debt collector text?

You may be contacted by Unifin for reasons associated with your past or current debts. The most common reasons for getting a text or a call from Unifin include:

- An unpaid or past-due debt that may have been assigned or sold to Unifin by your original creditor to collect on their behalf. This can involve credit cards, loans, consumer debts, or medical bills.

- An old account with a creditor, making it hard to remember an outstanding debt.

- A transferred or sold account that previously belonged to another company but was later acquired by Unifin, which now acts as the new collector.

- Incorrect contact information or mistaken identity that was assigned to you due to an error made during debt transfer, or that was entered incorrectly initially, or as a result of your phone number previously belonging to someone else.

Looking through the complaints filed against Unifin on the Better Business Bureau website, a U.S. business watchdog and scam-tracking source, it’s easy to see how many people are frustrated with unexpected communication from Unifin. Many Unifin Inc. reviews mention Unifin “harrassing” people with endless texts and calls while they have difficulty remembering the debt in question or claim they have no outstanding debts at all. While it’s Unifin’s job to contact debtors, mistakes do happen, and Unifin has been actively responding to frustrated customers, letting them know they’ve been placed on the Do Not Contact list and won’t be approached by the agency in the future.

Remember that getting a text alone can’t enforce debt payment on you or confirm that you owe a debt until you verify it by requesting an official debt validation notice from Unifin and checking your credit report.

How Unifin impersonators get your phone number

Not all Unifin debt collector texts and calls come from the real Unifin, though. Debt collection fraud is proliferating, as it appears to be a low-hanging fruit for scammers.

Unifin is yet another frequently impersonated debt collection agency. Scammers take advantage of existing data exposure by impersonating Unifin and targeting people whose phone numbers already appear to be connected to some sort of financial activity (which is almost everyone these days).

Like in the case of CCSPayment scams, fake Unifin debt collectors obtain their targets’ phone numbers from a range of free and paid sources:

- Public records are one of the simplest way to obtain someone’s information, for example, court filings, business registrations, property records, and more. That’s why, for privacy purposes, it makes sense to remove your public records from the internet, as well as review and remove your court records, if any.

- Data broker and people-search websites legally buy, aggregate, and publish contact information of millions of people. Scammers can scrape or purchase this information, including phone numbers, full names, home addresses, past financial activity, and more.

- Data breaches can expose personal data of millions of people at a time, especially if that data was submitted to large-scale retailers, SaaS companies, banks, or healthcare providers. For example, 4.4 million people were affected in the TransUnion data breach, exposing their names, phone numbers, billing addresses, birthdates, and even Social Security numbers.

- Online form submissions often contain phone numbers, including those belonging to businesspeople. When leaked or used with malicious intent, these submissions can become a rich source of personal information for debt collection scammers.

Is the Unifin debt collector text a scam?

Are all Unifin debt collector texts a scam? The answer is: it depends. Some texts are legitimate, but many impersonate Unifin in an attempt to steal personal and financial information from unaware people.

In many cases, people reported getting a voicemail or a message requesting that they call “Unifin” back using the provided phone number. This is a popular form of vishing, or voice-based phishing, forcing victims to get on a call with scammers who then use the opportunity to harvest sensitive data and banking details.

In some cases, scammers use a combination of methods, both texts and calls.

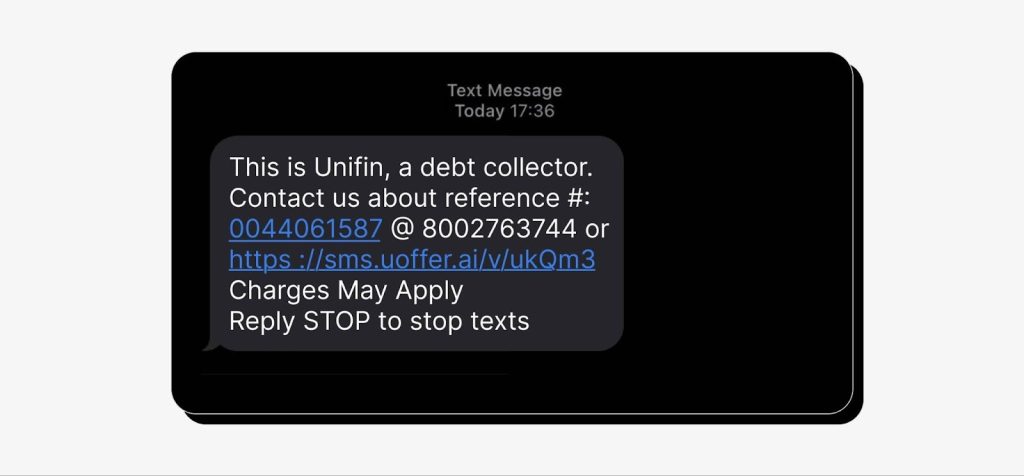

How do you tell if it’s a Unifin scam text? Some telltale signs are the following:

- It’s an unsolicited message, and you can’t recognize the debt in question. Sometimes it’s a sign your identity has been mistaken or your contact details confused, but in other cases it’s just a blanket scam campaign targeting hundreds of people at a time.

- There’s pressure to act quickly: such messages often feature short deadlines and claims that you must act now to avoid consequences.

- Threatening language that mentions legal action, wage garnishment, or arrest. No legitimate debt collector has the right to communicate in this way, so this is a prime sign of a scam.

- Shortened or unfamiliar links that don’t match Unifin’s official website domain, which is unifininc.com. Clicking these links can take you to spoofed websites that resemble Unifin’s corporate style but are only designed to steal your information.

- Requests for sensitive information. Right away, fake debt collectors may start asking for your SSN, date of birth, and banking details, either through phishing links in the scam text or over the phone. Remember that legitimate debt collectors may ask for your name and the last four digits of your SSN only after you have verified their affiliation with Unifin.

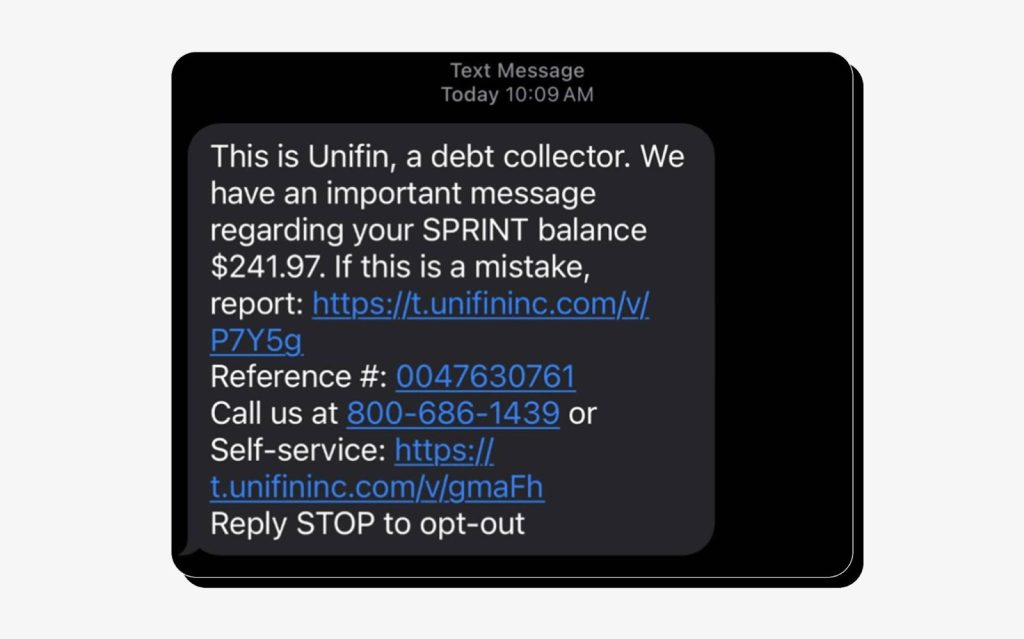

For reference, below is an example of a legitimate Unifin text. You can see that this message introduces Unifin as a debt collector and features important (and personalized) information regarding a particular debt, such as its outstanding amount and reference number. Note that the links provided are not disguised with a link shortener, there’s no pressure to act immediately, the message includes ample contact details, and there’s an opt-out option to stop these messages.

To sum up, here’s how a legitimate Unifin text message differs from a fake one:

| Legitimate Unifin text | Unifin scam text |

|---|---|

| Personalized | Generic |

| Solicited or features a recognizable debt | Unsolicited or features an unknown debt |

| Features a particular debt, its amount, and reference number | No debt specified apart from a generic reference number |

| Provides a self-service portal link with the unifininc.com domain | Links hidden behind link shorteners or spoofed domains other than unifininc.com |

| Provides a way to report if the message is a mistake | No way to report the text |

| Has no grammatical, spelling, or formatting errors | May contain grammatical, spelling, or formatting errors |

| Stops after opting out | Replying with STOP may intensify scam attacks |

How to verify a Unifin text message

If you receive a text claiming to be from Unifin, the first step is to pause and verify the information. Until you can verify the legitimacy of the message, it’s best to assume it’s a scam unless proven otherwise.

Pause and verify

As scam texts typically rely on urgency, do not reply, interact with the links, or call the phone number featured in the message. To verify the debt mentioned in the text, it’s recommended to reach out to Unifin directly, either by calling the Unifin debt collector phone number (1-888-572-3987 for English speakers and 1-800-556-0504 for Spanish speakers) or by filling in the request form on their website.

Another way to verify if you owe any outstanding debt is to check your credit report with one of the major credit bureaus (Experian, Equifax, TransUnion).

Check the sender number and format

Look at how the message is structured and the number it’s sent from:

- Is it a short code or an international number? If so, it’s a common sign of a scam.

- Does the message contain enough identifying details, such as your name, debt reference number, and the creditor/debt sum in question? Their absence may point to a scam.

- Does it look brief and professional, or is there poor grammar, weird formatting, and generic wording? The latter are common in scam messages.

Avoid links and payment requests

Don’t trust payment links or requests sent by text. If the message pushes you to enter your personal details, pay immediately, or verify information using the provided link, especially if it’s hidden behind a link shortener, it’s a major red flag.

These links may lead to a spoofed or phishing website that will steal the information you entered, which scammers can then use for identity and financial fraud.

What to do if you receive a Unifin debt collector text

Whether the text is legitimate or not, you don’t have to panic or act immediately.

If the Unifin message is legitimate

If the message looks professional, non-threatening, and you have verified your debt via Unifin’s official representatives:

- Request a debt validation notice. You have the right to ask for written debt confirmation stating the original creditor and the amount owed, which should be sent to you within 5 days of your request.

- Keep records. Save all letters, messages, and details shared in conversations with Unifin’s debt collectors to keep track of the timeline and negotiations.

- Don’t pay right away. You have the right to dispute the debt as well as negotiate its payment terms.

- Request to stop communication. You can also explicitly ask Unifin to stop contacting you. As a legitimate debt collection agency, they should exclude you from their contact lists in this case.

If the Unifin message is a scam

If you received a Unifin scam text:

- Don’t reply, interact with the links, or call the phone numbers listed in the message.

- Block the sender on your phone.

- Take screenshots of the sender ID and the message for reporting purposes.

- Report the message to your mobile carrier by forwarding it to 7726 (SPAM).

- File a fraud report with the Federal Trade Commission using the saved evidence.

- Notify Unifin about the impersonation scam directly so they know about it and can warn their customers.

Your rights when receiving debt collection texts

Remember that under the Fair Debt Collection Practices Act (FDCPA) debt collectors have clear limits on how they can and cannot communicate with you.

They are not allowed to:

- Harass or repeatedly contact you.

- Contact you before 8 a.m. and after 9 p.m.

- Threaten you with arrest, lawsuits, or wage garnishment.

- Use pressure, abusive or deceptive tactics to make you pay.

In addition, when using electronic means of communication, they should provide you with a clear way to opt out of being contacted.

Reduce debt collection scam risk by limiting personal data exposure

Is your phone number out there for scammers to see? Having your personal information freely available to bad actors via public records, Google search, or people-search websites makes you a more convenient target.

Use Onerep to remove your personal information from 310+ websites, reduce your identity exposure online, and enjoy knowing your phone number won’t be exploited by fake debt collectors.

FAQs

Is Unifin a legitimate debt collector?

Yes, Unifin is a legitimate debt collector and business process outsourcing company based in the USA. It collects debts on behalf of original creditors and can contact debtors as an authorized third-party debt collector.

What happens if I ignore a Unifin text?

If the Unifin text is legitimate, they are likely to keep contacting you while the debt remains unresolved. The text message is not a legal notice and doesn’t obligate you to respond immediately. If the text is a scam, you should ignore it, block the sender, and report it.

Can Unifin legally text me about a debt?

Yes, Unifin may use electronic means of communication, including text messages, to notify you about an outstanding debt. However, they should provide you with a way to opt out of such communication.

Can scam texts use real Unifin phone numbers?

Yes, scammers can use caller ID and number spoofing to display “real” Unifin phone numbers that redirect to the scammers’ phone line if you call back. They also use a range of convincing-looking U.S.-based numbers to make their message appear legitimate.

Mikalai is a Chief Technical Officer at Onerep. With a degree in Computer Science, he headed the developer team that automated the previously manual process of removing personal information from data brokers, making Onerep the industry’s first fully automated tool to bulk-remove unauthorized profiles from the internet.